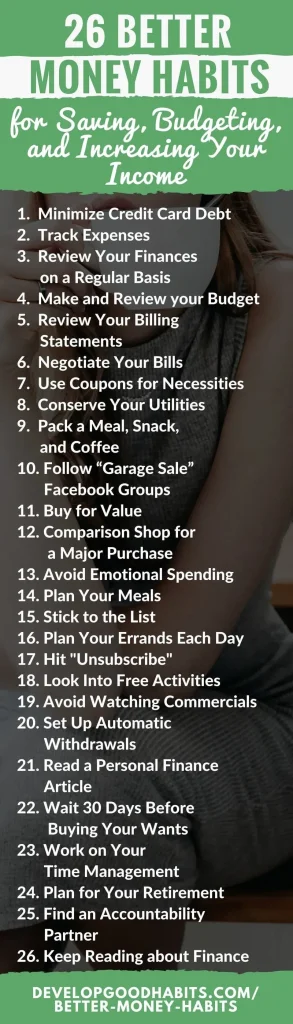

Money-saving habits are more than a quick thrift; they’re intentional patterns that accumulate financial strength over time. By embracing personal finance tips and budgeting strategies, you turn small actions into meaningful savings. Frugal living doesn’t mean deprivation; it means choosing value, planning meals, and track expenses to keep costs predictable. Even small steps, like setting up automatic transfers to save money, compound over time. With consistency, you create a sustainable system that makes mindful spending and long-term goals feel within reach.

Beyond the phrase money-saving habits, this topic can be framed as prudent money management and cost-conscious routines that protect your financial well-being. LSI-friendly terms like savings discipline, expenditure oversight, and long-range wealth building reflect the same idea from related semantic fields. Consider concepts such as an emergency fund, budget discipline, and value-driven spending to describe the path toward financial resilience. In practice, this shifts focus from strict restriction to purposeful planning, smarter purchases, and consistent progress toward future security.

Money-Saving Habits That Build Financial Resilience

Money-saving habits are more than a few frugal choices; they are intentional actions that, when repeated, compound into meaningful improvements in your finances. By embracing simple, repeatable routines—such as tracking expenses, reviewing where every dollar goes, and applying practical personal finance tips—you create a foundation for progress that can outpace sporadic windfalls. These habits transform budgeting from a restriction into a pathway to greater financial control and confidence.

Automating your savings turns intention into habit. Set up automatic transfers to a dedicated savings or emergency fund on each payday, starting with an amount you won’t miss. Over time, this set-it-and-forget-it approach helps you save money consistently and build a cushion that reduces stress during life’s surprises. This aligns with smart budgeting strategies that prioritize essentials, debt repayment, and built-in savings, making progress feel natural rather than forced.

Frugal living strengthens money-saving habits by infusing daily life with mindful choices—meal planning, smarter shopping, and deliberate consumption. Small shifts, like planning meals, checking unit prices, and avoiding impulse buys, compound into meaningful yearly savings without sacrificing quality or joy. Embracing frugal living as a habit supports long-term goals such as an emergency fund, debt reduction, and the freedom to invest in opportunities that matter most.

Budgeting Strategies and Frugal Living for Sustainable Wealth

Budgeting strategies redefine spending as a proactive plan rather than a constraint. A zero-based budget assigns every dollar a job before the month begins, aligning spending with priorities and embedding practical personal finance tips into daily decisions. By track expenses and compare actuals to the plan, you gain clarity and the power to adjust as life changes, ensuring your money serves your goals rather than the other way around.

Frugal living is about maximizing value, not deprivation. Begin with a careful audit of recurring costs—subscriptions, bills, and services you rarely use—and negotiate or switch to cheaper options. Shopping with a list, leveraging unit pricing, and using coupons strategically fit within a sustainable framework, helping you save money while maintaining a comfortable lifestyle. These steps, combined with disciplined saving, lay the groundwork for long-term wealth and financial resilience.

For long-term growth, couple steady budgeting with consistent saving and smart investing. Take advantage of retirement accounts, employer matches, and low-cost, diversified investments to let money compound over time. The key is time and consistency: even modest, regular contributions accumulate into substantial wealth, transforming everyday budgeting strategies into real financial security while supporting a frugal yet fruitful lifestyle.

Frequently Asked Questions

How can I apply personal finance tips and budgeting strategies to track expenses and start saving money?

Start by tracking expenses for 30 days to establish a baseline using a simple spreadsheet or budgeting app. Implement a zero-based budget so every dollar has a job—essentials, debt payments, savings, and discretionary spending. Set up automatic transfers to a savings account on payday to automate saving. Regularly review subscriptions and cancel unused services. Compare prices, negotiate where possible, and choose value over price. By making saving automatic and monitoring progress, small, consistent actions compound into meaningful money saved over time.

Which budgeting strategies and frugal living practices are most effective for building an emergency fund and saving money over time?

Focus on high-impact budgeting strategies and practical frugal living habits that sustain momentum. Use a flexible zero-based budget that prioritizes essentials, debt repayment, and savings. Adopt frugal practices such as meal planning, cooking at home, buying generic brands, and shopping with a list to reduce waste and costs. Automate monthly transfers to an emergency fund and other savings accounts, aiming for 3–6 months of essential expenses. Schedule a monthly money date to track expenses, review progress, and adjust as life changes. These steps help you save money consistently while maintaining quality of life.

| Section | Key Points |

|---|---|

| Introduction |

|

| Why money-saving habits matter |

|

| First steps: awareness and baseline tracking |

|

| Budgeting as a framework |

|

| Automate your savings |

|

| Cutting costs without sacrificing quality |

|

| Frugal living: smart habits for everyday life |

|

| Building and protecting an emergency fund |

|

| Debt reduction: leading with smart strategies |

|

| Smart saving strategies for long-term growth |

|

| Track, adjust, and celebrate progress |

|

| Life-stage adjustments and ongoing education |

|

| Common pitfalls and how to avoid them |

|

| Practical tips you can start today |

|

| Conclusion |

|

Summary

The HTML table above summarizes the key points from the base content on money-saving habits and provides a concise, readable layout. It highlights the rationale, practical steps, and long-term benefits of adopting money-saving habits, followed by a descriptive conclusion.