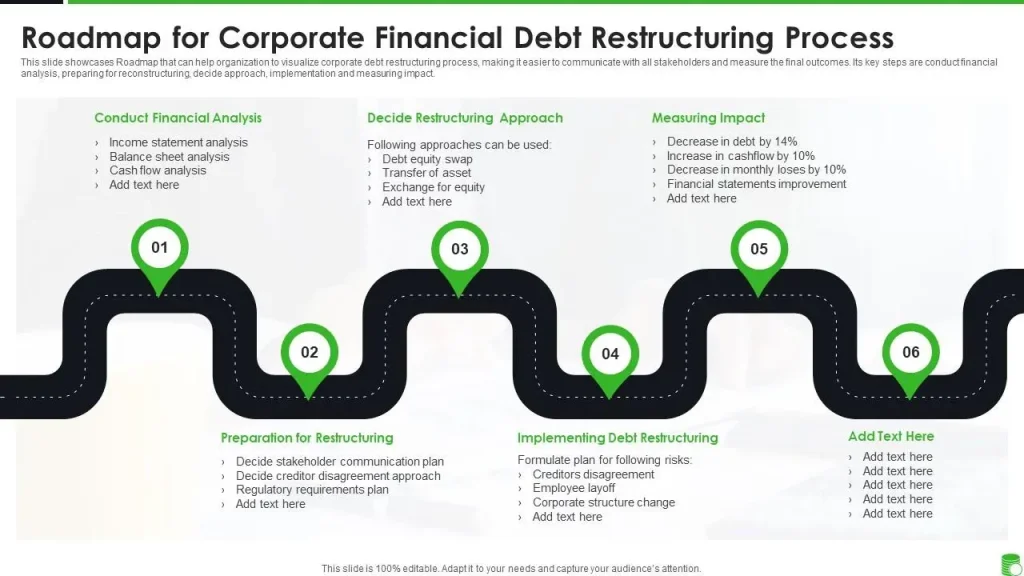

Debt Reduction Roadmap is a practical, step-by-step guide that turns a daunting debt load into a manageable project. With this framework, you translate debt payoff into concrete monthly actions, moving you toward a debt-free future. By inventorying what you owe, applying budgeting tips, and choosing debt payoff strategies, you build a practical path for ongoing financial health. The approach remains flexible and realistic, helping you adapt as life changes while staying focused on lowering balances. With clear milestones and steady motivation, you can shrink debt, protect your finances, and move toward lasting financial freedom.

From another angle, the concept can be described as a debt payoff framework, a repayment blueprint, or a financial reset that reorders your money priorities. Using LSI principles, we connect related ideas like monthly cash flow, interest savings, automated payments, and a disciplined budgeting approach to the same goal. Other terms you might hear include debt reduction strategy, debt consolidation option, and a solid personal finance plan, all pointing to a repeatable system for reducing balances. Ultimately, the focus is on sustainable progress, emergency fund growth, and long-term wealth-building as you follow the roadmap to financial resilience.

Debt Reduction Roadmap: A Practical Path to Debt-Free Living Through Smart Budgeting

Using the Debt Reduction Roadmap, you turn debt payoff into a concrete monthly action plan. This framework anchors your effort in a clear debt inventory, realistic budgeting, and a personal finance plan designed to move you toward debt-free living. By listing every balance, tracking monthly costs, and setting a target date, you transform anxiety into momentum and create a repeatable process you can revisit as circumstances change.

Step-by-step budgeting and a flexible payoff approach keep the plan practical. A traditional budgeting framework (like 50/30/20 or zero-based budgeting) helps you free up money for principal, automate payments, and avoid penalties. The Debt Reduction Roadmap also outlines debt payoff strategies—avalanche, snowball, or a hybrid—to fit your personality and finances, and it shows when debt consolidation might be sensible if it lowers costs without encouraging new debt. A dedicated emergency fund shields momentum when life happens.

Debt Payoff Strategies and Budgeting Tips: Accelerate Momentum with a Personal Finance Plan

Effective payoff begins with clear strategies and practical budgeting tips. The Debt Reduction Roadmap emphasizes debt payoff strategies such as avalanche or snowball, integrated into a broader personal finance plan. By prioritizing high-interest balances and creating a payoff fund within your budget, you can reduce total interest, shorten timelines, and maintain everyday living costs.

To sustain progress, combine ongoing tracking and flexibility. Recalculate timelines as debts disappear, automate payments, and consider debt consolidation when appropriate to simplify management and potentially lower rates. Keeping your personal finance plan adaptable helps you celebrate small wins, avoid common pitfalls, and stay debt-free long-term.

Frequently Asked Questions

How can the Debt Reduction Roadmap help me become debt-free while applying practical budgeting tips?

The Debt Reduction Roadmap guides you from a clear debt inventory to a sustainable budget and a chosen payoff strategy, making debt-free status achievable. It blends budgeting tips with proven debt payoff strategies (avalanche, snowball, or a hybrid) to reduce principal faster while protecting day-to-day needs. By automating payments, tracking progress, and using a dedicated payoff fund, you can accelerate results and stay motivated on the path to debt-free living.

What is the role of debt consolidation and a personal finance plan within the Debt Reduction Roadmap?

Debt consolidation can be a tool within the Debt Reduction Roadmap if favorable terms exist; however, it isn’t a cure for debt. It merges multiple debts into one payment and may lower your interest rate, but you should weigh fees and the effect on credit. The Debt Reduction Roadmap also supports a broader personal finance plan by aligning debt payoff with savings, investing, and risk management, so consolidation should fit within your overall strategy.

| Aspect | Focus / What it covers | Key Actions / Takeaways |

|---|---|---|

| The Debt Reduction Roadmap (Overview) | A practical framework to translate debt payoff into concrete monthly steps. | Inventory what you owe, budget effectively, choose a payoff strategy, and stay motivated. |

| Step 1: Get a Clear Picture of Your Debt | Inventory debts and monthly costs; establish a baseline. | List every debt type; gather balance/minimum payment/interest/date; create a debt inventory; calculate total monthly minimums. |

| Step 2: Build a Sustainable Budget | Budget as the engine to fund living expenses, savings, and payoff. | Identify income/expenses; cut discretionary costs; choose a budgeting framework; create a payoff fund; automate payments; plan for irregular income. |

| Step 3: Choose a Payoff Strategy | Decide which balances to tackle first and how fast. | Use Avalanche, Snowball, or Hybrid; consider penalties/fees and balance transfers; pick a sustainable approach. |

| Step 4: Accelerate Payoff with Smart Moves | Make payoff progress faster with smarter payments. | Biweekly payments; apply windfalls; refinance/consolidate when sensible; gradually increase payments; cut recurring costs. |

| Step 5: Consolidation & Negotiation | Levers to simplify payments and potentially reduce costs. | Debt consolidation loan; balance transfers; creditor negotiations; caution about pitfalls. |

| Step 6: Build an Emergency Fund | Protect momentum from debt payoff disruptions. | Target 1-3 months of essential expenses; treat as a separate savings goal; reassess as momentum grows. |

| Step 7: Track Progress & Stay Motivated | Keep the roadmap dynamic and life-responsive. | Set monthly milestones; recalculate timelines; review budget; visualize progress. |

| Common Pitfalls | Common mistakes to avoid on the road to debt freedom. | Relying on minimum payments; ignoring interest; inflexible planning; impulse purchases. |

| Mindset & Momentum | The human side of sustained debt payoff. | Set clear goals; seek accountability; track non-monetary progress; use visualization to stay resilient. |

| Beyond Payoff | Building a broader personal finance foundation beyond debt payoff. | Emergency savings, retirement planning, investing, insurance, and a flexible life plan. |

Summary

Debt Reduction Roadmap is a realistic, repeatable framework for paying off debt and achieving financial freedom. By starting with a clear debt inventory, building a sustainable budget, selecting a payoff strategy, and accelerating payoff with smart moves, you can shorten payoff timelines, reduce interest costs, and build a solid financial foundation. The roadmap is adaptable for different situations—whether you carry a few cards or multiple loan accounts—emphasizing motivation, accountability, and ongoing adjustments. With commitment to the Debt Reduction Roadmap, debt-free living becomes feasible and sustainable, setting the stage for emergency savings, wealth-building, and resilient finances for life.