Investing for Beginners is not about chasing fast gains or trying to predict every market twist, but about building a reliable, repeatable process that steadily grows your wealth over time through disciplined saving, broad diversification, and a commitment to ongoing learning. By focusing on investing basics and practical beginner investing tips, you can set up a simple, long-term plan that aligns with a sensible long-term investment strategy and smart financial growth, and this approach translates theory into action by prioritizing low costs, regular contributions, and a diversified mix that can weather different market environments. Starting with small, disciplined steps, such as automating contributions, keeping costs low, and staying patient, helps you translate earnings into meaningful progress toward your financial goals, while building good habits that survive market noise, maintain discipline during drawdowns, reinforce your confidence in the investing journey, and reduce decision fatigue by clarifying priorities across time. A clear path exists, and you can begin with a manageable monthly plan that scales from a modest $50 to a diversified portfolio as your circumstances evolve, supported by a simple tracking method, a routine review, and a mindset that rewards consistency over timing, while documenting milestones and benchmarks for progress. Let this overview serve as your roadmap to confidence and competence in investing for beginners, with a focus on steady growth, practical, real-world results, and a commitment to learning from mistakes, refining your strategy, and gradually increasing your influence over your financial future, so you can look back years from now and see tangible progress toward financial independence.

From an alternative perspective aligned with LSI principles, entry-level investing emphasizes understanding how assets, risk, and time work together to build wealth. The focus shifts from chasing headlines to mastering core ideas such as asset allocation, diversification, cost awareness, tax efficiency, and automatic contributions that support a steady compounding process. This reframing uses related terms like starter investment journey, beginner finance basics, and long-range wealth planning to connect practical steps with the broader semantic map of smart financial growth.

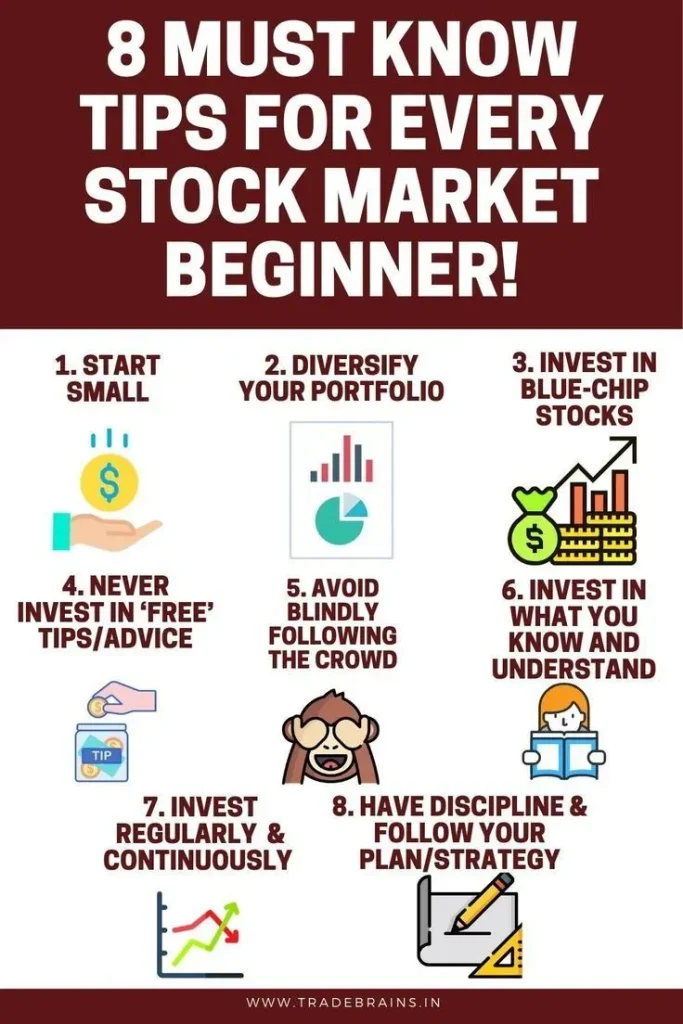

Investing for Beginners: Build a Stable Foundation for Long-Term Investment Success

To start confidently, focus on investing basics that protect you in downturns and position you for steady compounding. Begin with an emergency fund and a plan to reduce high-interest debt; these moves safeguard your capital so you won’t be forced to sell during market dips. A simple budget and a clear savings plan lay the groundwork for beginner investing tips that translate into lasting wealth, and they support a true long-term investment strategy centered on disciplined contributions and low costs.

Once you have a safety net, automation and a sensible asset mix help you turn intentions into action. Dollar-cost averaging—investing the same amount regularly—reduces timing risk and leverages compounding. Choose low-cost, broad exposure through index funds or ETFs, align your allocation with your time horizon, and rebalance as needed to maintain your target risk level. This is a practical approach to smart financial growth that scales from a small monthly plan into a diversified multi-portfolio strategy over years.

Core Practices for Sustainable Growth: Dollar-Cost Averaging, Costs, and Diversification

Deliberate execution beats market guessing. Emphasize diversification across asset classes (stocks, bonds, cash equivalents) and geographies to smooth volatility and protect you from single-name risk. Keep costs in check by favoring low-fee funds, and be mindful of taxes and account types that influence after-tax growth. This aligns with investing basics and supports a long-term investment strategy focused on consistent contributions and principled spending.

With a plan in place, your daily, weekly, or monthly habits matter. Automate contributions, monitor risk tolerance as life changes, and rebalance periodically to preserve your intended mix. A thoughtful approach to beginner investing tips, paired with a long-term perspective, helps you translate small, regular investments into meaningful growth while reducing decision fatigue and avoiding costly mistakes.

Frequently Asked Questions

What is Investing for Beginners, and how can I apply investing basics to build a long-term investment strategy?

Investing for Beginners is a steady, disciplined path to grow wealth over time, not a quest for quick wins. Start with investing basics: build an emergency fund, set clear goals, and choose low-cost, broad-market funds such as index funds or ETFs to create a diversified core. Use a long-term investment strategy that emphasizes regular contributions (dollar-cost averaging) and periodic rebalancing to maintain your target risk. By staying patient and keeping costs low, you can achieve smart financial growth through consistent, repeatable steps.

What beginner investing tips can help me achieve smart financial growth while keeping costs and risks in check?

Key beginner investing tips include focusing on a core diversified portfolio of index funds or ETFs, adding bonds for balance, and automating contributions to practice dollar-cost averaging. Keep costs low by avoiding high fees and minimizing unnecessary trades, and use tax-advantaged accounts where available to boost after-tax growth. Define your time horizon and risk tolerance to guide your asset allocation and rebalance regularly so you stay aligned with your long-term investment goals. Start small, stay consistent, and let compounding work over time to deliver smart financial growth.

| Topic | Key Points |

|---|---|

| Foundations for Beginners | Emergency fund (3–6 months), pay down high‑interest debt, and set a realistic budget and savings plan. |

| Goals and Time Horizon | Define goals and time horizon; short‑term needs vs retirement; horizon informs risk tolerance and asset mix; longer horizons allow more growth. |

| Core Concepts: Diversification, Costs, and Tax Implications | Diversify across asset classes; keep costs low with broad funds; understand how taxes affect after‑tax growth and use tax‑advantaged accounts where possible. |

| Starting Your Investment Plan: Vehicles and Allocation | Use a core‑satellite approach with broad‑market index funds/ETFs as the core; add targeted positions as needed; include bonds for risk control; allocation depends on goals and time. |

| Asset Allocation and Rebalancing | Create a dynamic plan and rebalance periodically to maintain target risk; sell what has grown and buy what has lagged. |

| Dollar‑Cost Averaging and Automation | Automate regular contributions; invest a fixed amount on a schedule to reduce market timing and enforce discipline. |

| Accounts and Tax‑Advantaged Vehicles | Favor tax‑advantaged retirement accounts (e.g., IRA/401(k)) when possible; use taxable accounts as flexibility; prioritize low‑cost broad exposure. |

| Portfolio Design: Risk Profiles | Conservative: ~60% bonds / 40% stocks; Balanced: ~60% stocks / 40% bonds; Growth: ~80% stocks / 20% bonds; prefer broad funds within stocks. |

| Risk Management & Behavioral Considerations | Behavior matters as much as math; set rules to resist emotional moves and align decisions with goals and risk tolerance. |

| Common Mistakes for Beginners | Paying high fees, market timing, lack of diversification, and ignoring taxes; counter with low costs, automation, broad diversification, and tax awareness. |

| Taxes, Accounts, and Long‑Term Growth | Account types determine after‑tax results; tax‑advantaged accounts support long‑term growth; understand local rules and plan for taxes. |

| A Simple Everyday Routine for Your Journey | Set monthly contributions and automate; review goals and rebalance annually; reinvest dividends; stay low‑cost and diversified. |

| Practical Tools and Resources for Beginner Investors | Use reputable, low‑fee brokers; leverage online calculators and fund reports; start small and increase contributions. |

| Case Study: A Realistic Path to Retirement Savings | Example: a 25‑year‑old saves $300/month in a diversified, low‑cost portfolio and compounds for decades; outcome depends on market, fees, and contributions. |

| Putting It All Together: Your 6‑Minute Daily Practice | Review contributions, rebalance if needed, read/watch a short educational item, reflect on goals, and celebrate small wins. |